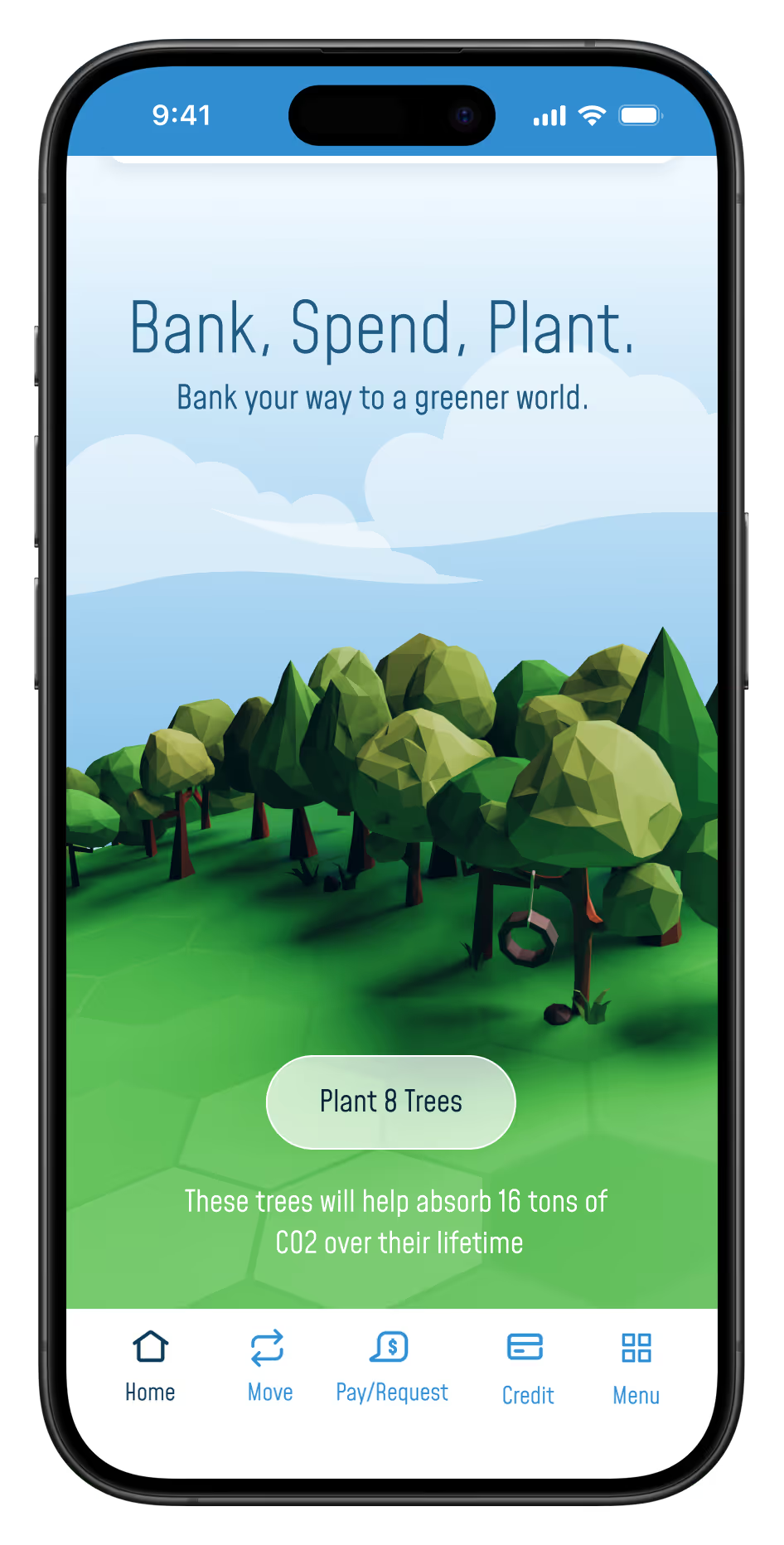

Bunq

Dutch NeoBank - Reimagined for an American Market

PROBLEM

Dutch Neobank has been having trouble breaking into the American marketplace due to cultural differences in need.

TARGET

Rethink their app and brand to appeal to American sensibilities and target a 3X increase in membership.